Under Section 121 of the IRS Code, and spelled out in IRS Publication 523 (2013), homeowners who sell their primary residence may be able to exclude from income any gain up to a limit of $500,000 if the homeowners are married and file a joint tax return. The limit is $250,000 for a single income tax filer or a married Read More >

What Are Lenders Looking For? Collateral!

Posted on: 10.27.14

When a lender is confronted with a borrower seeking financing they are looking for the 4 Cs of borrowing. In a post entitled “What is the Greatest Obstacle to Borrowing Money to Purchase a House?” I explained what the 4 Cs of borrowing are. In this post I intend to get much more specific as to what a lender is looking Read More >

Time to Pay the Piper – What are Required Minimum Distributions?

Posted on: 09.30.14

Let’s review. Up to this point you’ve been contributing pre-tax dollars to a qualified plan. The money in your qualified plan has been increasing and decreasing based on the performance of the investments you have chosen in your plan. You have deferred the taxes due on the dollars you contributed to the plan as well as Read More >

Borrowing from Your Qualified Plan – The Good, the Bad, and the Ugly!

Posted on: 09.28.14

In these challenging economic times, an increasing number of Americans are borrowing money from their qualified plans to bridge the gap between their cash inflows and outflows. In fact, according to HelloWallet.com, more than one in four Americans have done this, using the money to pay mortgage payments, credit card Read More >

At What Age Does Tax Law Permit You to Withdraw Money from a Qualified Plan?

Posted on: 09.25.14

If you said 59 ½, you’re wrong. If you said 70 ½, you’re wrong. The truth is it’s a trick question. The correct answer is: Tax law lets you withdraw money whenever you want, regardless of your age. Withdrawal means permanently removing money from your account. The IRS doesn’t care when you withdraw the money. Read More >

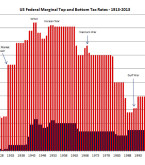

Is Postponing Tax Really the Best Idea?

Posted on: 09.23.14

Let’s say you wanted to borrow $10,000. What questions would you ask and want to know the answers to before you borrowed the money? I can think of at least two key questions, and probably more. What is the interest rate? How much interest do you have to pay? What is the payment? If the lender responded by Read More >