If you’re like most people who I ask that question, you said “All of it!” But is that true? Remember, you have elected to defer paying the tax. Let’s look at an example. Assume you are in a 30% tax bracket and you wish to make an annual contribution of $6,000 to your qualified plan. The best anyone could and should Read More >

The Value of an Employer Matching Contribution

Posted on: 09.16.14

Many employers that offer qualified plans will partially or fully “match” each employee’s contribution to the plan. Not all employers offer a match, but many do, and the match amount and terms can vary widely among employers. A typical match scenario might look like this: Employer will contribute 50% of the employee’s Read More >

What Do Qualified Plans Do?

Posted on: 09.09.14

Qualified plans do several things: They make it easy to save for retirement. They offer the opportunity to receive an employer match on your contributions. They defer otherwise payable income taxes. They defer the income tax calculation. Let’s evaluate each one individually. ⇒ Qualified plans make it Read More >

What is a Qualified Plan and How Does It Work?

Posted on: 09.02.14

401(k)s & IRAs belong to a class of retirement vehicles called Qualified Plans. By meeting the requirements of Section 401 of the Internal Revenue Code, 401(k)s qualify for certain tax treatment, the most significant being that both employer and employee contributions are tax-deductible in the year they are made, Read More >

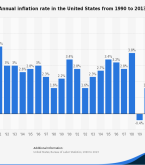

Money Isn’t Math and Math Isn’t Money – The Impact of Inflation

Posted on: 08.26.14

Money is a commodity. It changes in value and can erode over time. Math does not change, which is why we can never make the two synonymous. Let’s explore the impact that inflation has on our daily lives. Inflation has been called many things over time (i.e., a hidden tax, the silent killer, etc…), but what is it Read More >

Money Isn’t Math and Math Isn’t Money – Recovering from Market Losses

Posted on: 08.19.14

Can you recover from stock market losses? That depends on what context you use the word recover. Most people do not realize how much time and money it can take to recover from a steep market dive such as those experienced from 2000 – 2002 and 2007 - 2009. The S&P 500 stock index lost an estimated 46% of its value Read More >