According to the Employee Benefit Research Institute, approximately 42% of Americans in the private sector (i.e., non-government workers) are covered by a defined contribution plan such as a 401(k) or IRA. For many that contribute to these types of retirement plans, the primary benefits are the perceived tax savings and the potential for a company matching contribution.

The only way to save taxes utilizing tax deferral programs is to be in a lower tax bracket when you take the money out of the account than you were in when you put the money in the account.  For example, if you are in a 15% tax bracket when you retire and you were in a 25% tax bracket when you made the contributions, you win. If the opposite is true and you are in a 25% tax bracket when you retire and you were in a 15% tax bracket when you made the contributions, you lose.

For example, if you are in a 15% tax bracket when you retire and you were in a 25% tax bracket when you made the contributions, you win. If the opposite is true and you are in a 25% tax bracket when you retire and you were in a 15% tax bracket when you made the contributions, you lose.

Too many Americans focus on the tax bracket they are in today and not the tax bracket they will be in when they take the money out as retirement income. And that is where the problem lies. How can you know what tax bracket you’ll be in when you retire? The answer is you can’t. So we are left to guess.

So let me ask you. What do you believe future tax rates will be?

- Lower

- Higher

- Same

Your answer is your own, but if you’re like most people, you said higher and I happen to agree with you.

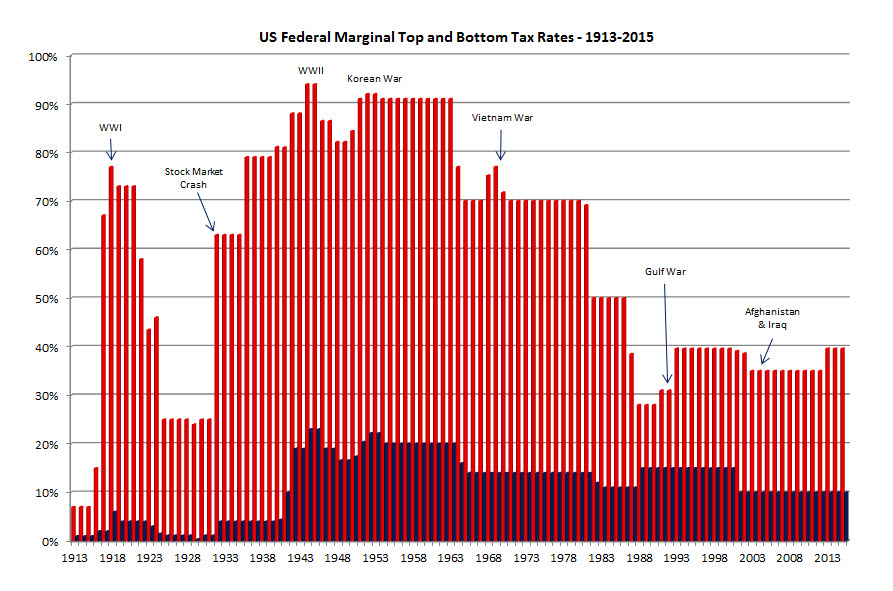

The graphic below shows the tax rates from 1913 to 2015. The top tax rate is in red and the bottom tax rate is in blue. It also shows many of the major events that influenced tax policy during that time period.

When 401(k)s and IRAs first appeared in the ‘70s it made perfect sense to contribute because the top tax rate was 70%. There was a strong likelihood that tax rates in the future would be lower. And that’s exactly what happened. In the early ‘80s the top tax rate dropped to 50%, and ultimately to 28%.

To the surprise of many Americans, we are in the lowest tax rate environment, historically, that we’ve been in since the 1980s. Since the income tax was instituted in 1913, the only times tax rates have been lower is from 1913 – 1916, 1924 – 1931, and 1988 – 1993.

According to www.USDebtClock.org, as I write this blog post the United States is just over $18.3 TRILLION dollars in debt. Outstanding student loan debt totals $1.4 TRILLION and outstanding credit card debt is $905 BILLION. We have municipalities like Detroit, Chicago, and Orange County on the brink of bankruptcy, which will require a bailout by the federal governemnt. We are facing a Medicare and Social Security crisis that is being strained further as 80 to 85 million Baby Boomers (those born between 1946 and 1964) retire over the next 20 years at the rate of 10,000 per day, according to the U.S. Census Bureau.

There are fewer and fewer workers contributing to Social Security and Medicare as more and more retireees collect those benefits for longer and longer periods of time. In 1935, when Social Security was enacted, there was approximately 42 workers contributing to Social Security for every 1 retiree receiving Social Security benefits. According to the newly released 2015 Social Security Trustees Report, there are 2.8 workers contributing to Social Security for every 1 retiree receiving benefits and the number of contributors per recipient will continue to drop.

There are fewer and fewer workers contributing to Social Security and Medicare as more and more retireees collect those benefits for longer and longer periods of time. In 1935, when Social Security was enacted, there was approximately 42 workers contributing to Social Security for every 1 retiree receiving Social Security benefits. According to the newly released 2015 Social Security Trustees Report, there are 2.8 workers contributing to Social Security for every 1 retiree receiving benefits and the number of contributors per recipient will continue to drop.

The government can only fund its activities through taxes and/or borrowing. Congress couldn’t raise taxes during the Great Recession (the housing and mortgage crisis and the stock market crash). So what did Congress do? They borrowed over $10 TRILLION to pay for it all. They put it on a credit card. However, in 2013, the President ended the 10th year of the 35% top tax rate and added a top tax rate of 39.6%, and it hasn’t even eliminated the annual deficit, let alone pay back any of the national debt. The writing is on the wall. Higher taxes are coming. The question is what are you going to do about it?

If you believe tax rates will be higher when you retire and you would like to discover strategies to protect your future income and lifestyle from the impact of higher taxes call us to discuss your specific situation.